You have AARI Metsä Oy's first market review in your hand. In our review, we will focus on the most essential issues for the forest owner and society. The leading topic of this review is the wood trade, the price level of wood and the functionality of the wood industry, as well as future prospects.

The price level of wood

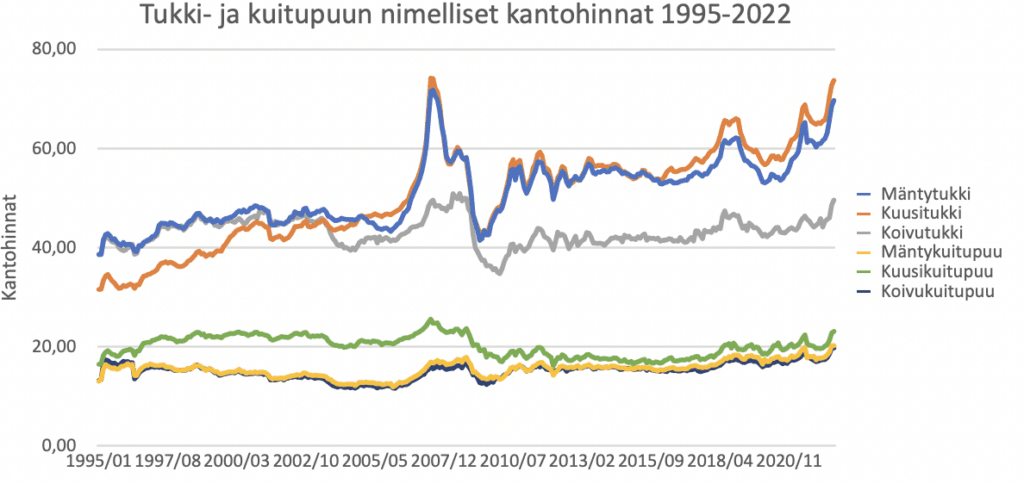

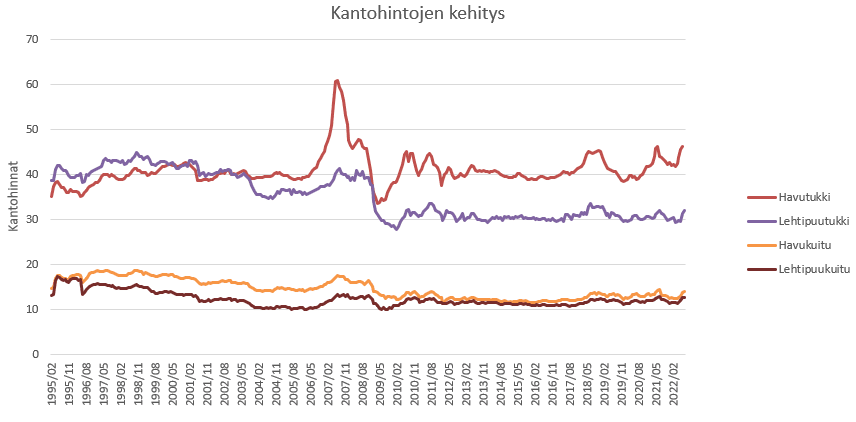

The price level of log wood rose by about 25% in the last two years. In the perspective of the last 10 years, the price peak of the summer 2022 was quite good. But if the price of log wood is compared to the record price level of lumber and for real-time wood price developments in the last two years, the experienced price peak was a slight disappointment.

he prices of regeneration felling log wood clearly improved and the forest owner also got a share of the increase in the value of the end products. The demand and price of conifer log correlate very strongly with economic cycles and especially construction activity. Our estimate is that the construction sector worldwide will enter a deep recession in the next six months and new construction project starts will fall to record low levels. Due to this, we estimate that the price of log wood will continue to fall for at least the next 6 months, and the price levels seen last spring will be reached in two years at the earliest. In the long run demand trends towards ecological materials and deforestation as well climate goals predict a strong price development for log wood as well, and we see significant growth potential in the price of wood.

Forest industry in Finland

In terms of the forest industry a clearly bigger structural problem in Finland is the chronically low price level compared to the demand and processing value of pulpwood, which unfortunately the forest owners have already used to.

As a result of the structural change in the paper industry, the price of pulpwood fell significantly in Finland in the early 2000s and remained at its low level. Until 2017, this low price level was also justified in terms of the legality of the market economy. The growth of forests clearly exceeded the demand for wood, there was more supply than demand, especially for pulpwood. However, the biofactory that was completed in 2017 in Äänekoski significantly balanced the situation, and other investments in recent years will change the situation to the opposite. Especially the pulp mill in Kemi, which will be completed next year, will increase the demand for pulpwood.

These investments have been a very patriotic act by Metsä Group, and many thanks and congratulations for that. Along with the love of the home country, the background of the investments is the global capitalist equation; Due to the functioning wood industry, the low price level of raw wood and Finland's excellent infrastructure, the price of pulpwood delivered to the mill is very competitive. Furthermore the demand for conifer pulp is growing globally faster than for broadleaf pulp i.a. due to the increasing use of packaging products. Areas of fast forest growth, such as South America, grow mostly broadleaf.

Wood price development in the future

When we add to the equation the drastically increased demand for energy wood and the increasing importance of forests as a carbon sink, we end up with a very simple equation: The global increase in wood fibre materials as a substitute for plastic and non-renewable materials and the rise in the price of energy especially increase the demand for pulpwood. Correspondingly, the increasing importance and benefits of forests as carbon sinks and as the preservers of biodiversity causes pressure on the supply of wood. In a market economy, growing demand always inevitably raises prices. If, on the other hand, the supply does not rise very sensitively when the prices rise, the price of the commodity can rise very high. A good practical example of this is the oil market. If the price increase did not occur in that situation, the only possible conclusion is that the market economy does not work.

Industry and use of wood

Forest industry companies used a total of 72.2 million cubic meters of lumber in 2021 in Finland. The use of domestic lumber increased by nine percent from 62.4 million cubic meters. There was growth in all types of timber.9.8 million cubic meters of imported lumber were consumed, which was one percent more than the previous year. Of the different types of wood, pine pulpwood (17.9 million m³) and broadleaf pulpwood (13.6 million m³) and spruce logs (14.4 million m³) were used the most. Log wood consumed a total of 27.3 million cubic meters (+11% from the previous year) and pulpwood 42.2 million cubic meters (+6%).

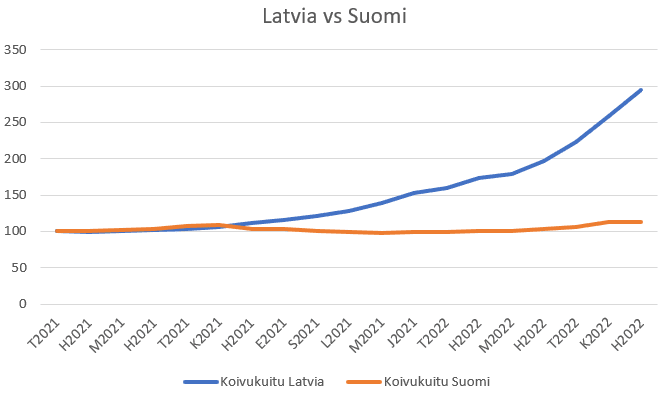

The share of birch imported from Russia in 2021 was 4.58 m³. According to the latest National Forest Inventory (NFI 12), the growth of birch in our country is about 19 million cubic meters and 10 million are felled. Imported birch can therefore be replaced with domestic birch. Birch can be bought domestically when the price level reacts to increased demand and reduced supply through the end of Russian imports. So far, this has happened in the Baltics, but not in Finland. Historically, price movements in the Baltic market have of course been clearly greater than in Finland, but such a significant difference in the graph below cannot be explained by normal cyclical fluctuations.

The future of Finnish wood

he demand and price trend for end products made from Finnish pulpwood is rising, but the real price of Finnish pulptwood is still falling and it is at a historically low level. In 1999, a forest owner who looked forwards to trends could perhaps foresee that the price of pulpwood, and especially birch fibre, would not remain at the same good level as in previous decades. Now in 2022, a forest owner who looks forward to trends and believes in the market economy can conclude that it is very likely that we will see a significant level increase especially in pulpwood, in the next few years, if not already in the next few months. There is an extremely valuable natural resource in Finland: a Finnish tree grown in a suitably calm and responsible manner. With the prevailing trends, the value of this material will rise higher and higher and it will generate interest steadilyevery year by growing its roots in the ground.

In summary, we anticipate that the price of log wood will decrease and the price of pulpwood will increase in Finland in the next 6 months. However, according to our estimate, the overall effect on the wood price level is negative and the price of an average stand marked for harvesting may even decrease in the following months. In the long term, we are very positive about the value development of wood and forest land and we see this as an asset class where global trends strongly support positive price development.

For the customers of AARI Metsä Oy and the sister company Conifer Consulting Oy, we have carried out wood sales earlier than normal, and the 2023 final felling lots have already been mostly sold for all customers. We see a clear upward price pressure in fiberwood-dominated thinnings, and for these, the main focus of the wood trade will be next year.